Executive and Non-executive Directors: Tax Matters

Categories:

Date Posted:

August 12, 2024

Written by Roulon du Toit CA (SA)

Both executive directors and non-executive directors (NEDs) may earn income from the companies in which they hold office. However, the tax treatment of these earnings—and the related expenses incurred—vary greatly between these two types of directors.

In 2017, SARS released two Binding General Rulings (numbers 40 and 41) which provided more clarity on the treatment of NEDs.

In this blog entry we’ll look at the tax treatment of both executive and non-executive directors under these headings:

-

Employees’ tax

-

Income tax

-

VAT

First, let’s start by discussing the definition of a NED in context of South African tax laws.

There is no definition for a NED in the Act. In Binding General Ruling 40, SARS makes reference to the characteristics of NEDs listed in the King III report which indicates that it is a person who is independent of, and not involved in, management of the company.

Binding General Ruling 40 further states that SARS considers a NED to be a “director who is not involved in the daily management or operations of a company, but simply attends, provides objective judgement, and votes at board meetings.”

An executive director is therefore a director which is involved in the day-to-day management of a company.

EMPLOYEES’ TAX

The Fourth Schedule to the Income Tax Act contains the employees’ tax legislation. This is the part of the Act that governs the calculation of Pay As You Earn (PAYE). Central to this are the definitions of “remuneration”, “employee” and “employer”. Without going into excessive detail, it is important to understand PAYE is only calculated on remuneration paid by an employer to an employee.

SARS accepts that a NED is not considered an employee in terms of the common law. Consequently, amounts paid to them by the company are not considered “remuneration”. Payments made by a company to a NED will therefore not be subject to employees’ tax.

The opposite applies to executive directors—payments made by companies to executive directors do fall under “remuneration” as defined and is therefore subject to employees’ tax. This is calculated in a similar manner to any other employee.

INCOME TAX

First, a note on “gross income”. Per paragraph (c) of the definition in section 1 of the Income Tax Act, amounts received by a person in respect of services rendered must be included in the taxpayer’s gross income. This makes it clear that amounts received by either executive directors or NEDs in respect of services rendered to the company will be included in their “gross income”.

But what of tax deductions which may be allowed against this income? Here it is important to consider section 23(m). Section 23 contains a list of prohibited deductions and subparagraph (m) specifically addresses taxpayers who earn mainly remuneration.

The subparagraph indicates that there are only a handful of expenses, relating to employment which may be allowed as deductions against gross income. In short, these expenses are legal costs, bad debts and provisions for doubtful debts, wear and tear, retirement fund contributions and expenses and repairs relating to a home office.

An executive director may, therefore, only deduct the expenses listed above in the calculation of their taxable income.

As noted previously, a NED does not earn “remuneration”. Therefore, section 23(m) does not apply to them. This means that a NED can claim expenses incurred in the production of income which may not otherwise be allowed under section 23(m).

Let’s use a simple illustration:

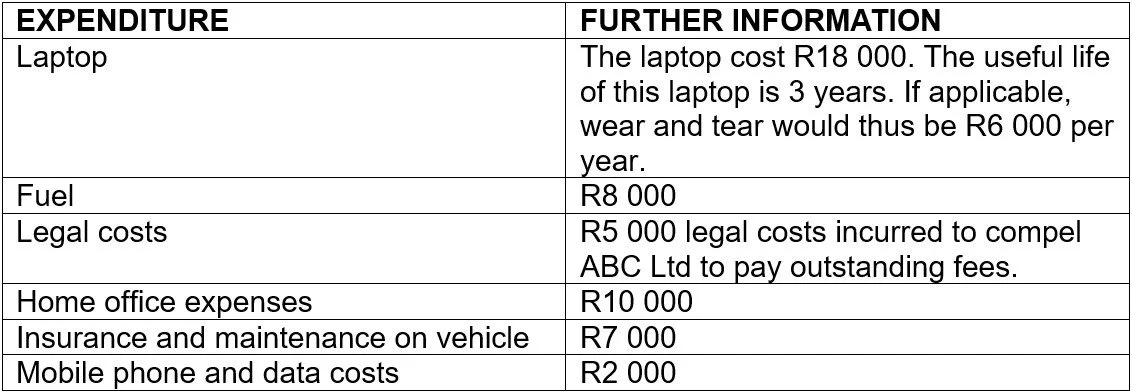

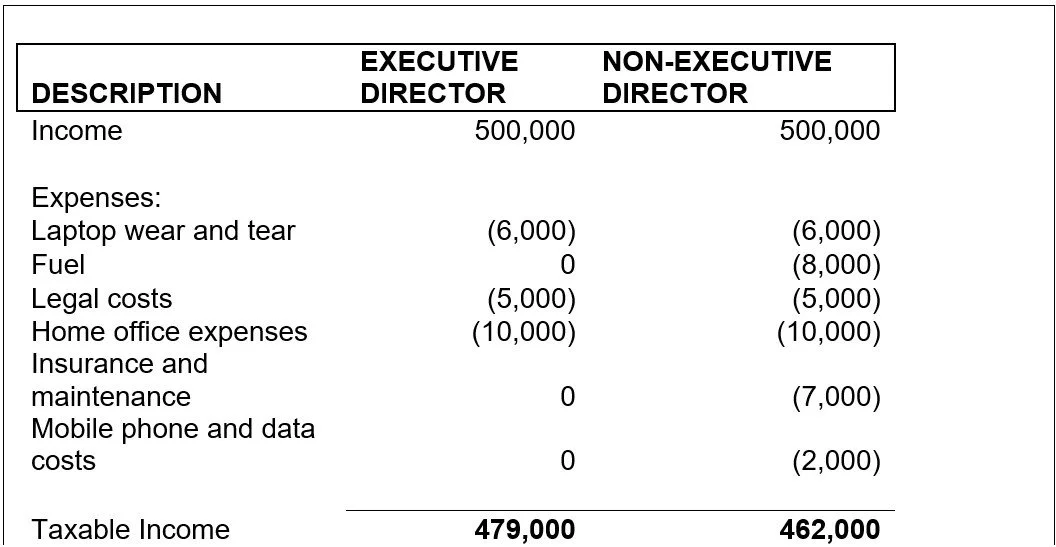

X is a director of ABC Ltd. X earns R500 000 from the company. Below is a list of expenditure incurred by X. For purposes of this illustration, assume that it is all directly incurred in the production of income.

What would be the impact on the calculation of taxable income if

a) X is an executive director

b) X is a non-executive director

In the above illustration, as an executive director the taxpayer would be earning “remuneration” and tax deductions would be limited in terms of section 23(m) . As a NED the taxpayer does not earn “remuneration” and section 23(m) is not applicable, resulting in more expenses allowed as a deduction.

VAT

In Binding General Ruling 41, SARS sets out its views on VAT and NEDs.

The VAT Act compels taxpayers who are carrying on an “enterprise” generating supplies of R1 million or more to register as a VAT vendor. The definition of an “enterprise” specifically excludes amounts which are considered “remuneration” in terms of the Fourth Schedule.

Executive directors earn “remuneration” and therefore they are not considered to be carrying on an “enterprise” for VAT purposes. Consequently, they should not, and cannot, register as VAT vendors. A NED does not earn “remuneration” and therefore they are considered to be carrying on an “enterprise”.

Consequently, a NED who earns R1 million must register as a VAT vendor and levy output tax on their fees to a company. These taxpayers must also submit VAT returns to SARS and comply with the administrative duties of VAT vendors, such as the requirement to submit VAT invoices and retention of records relating to input tax claimed. Failure to do so will lead to significant penalties and interest.

Once registered as a VAT vendor, a NED will also be able to claim input tax on expenses incurred in relation to their duties.

It is also worth mentioning that a person who is carrying on an enterprise where their supplies exceed R50 000 per year can voluntarily register as a VAT vendor.

Whilst an executive director is treated similar to other employees it is important to be aware that there are significant income tax and VAT consequences for being a non-executive director.